Show summary Hide summary

Ford has rolled out an unexpected financing move: low-rate loans usually reserved for prime borrowers are now available to buyers with weaker credit — but only on F-150 pickups. The promotion has stirred heated debate online and raised questions about pricing, inventory and the risk of more repossessions.

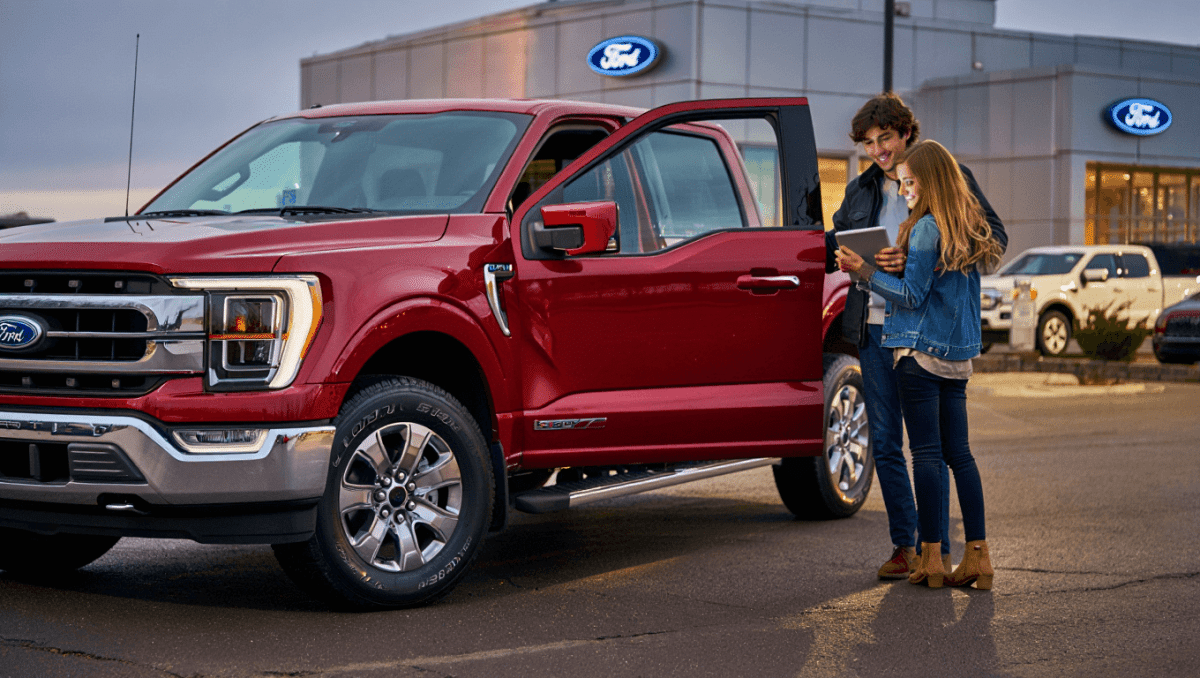

What the F-150 financing promotion actually offers

Ford Credit is temporarily extending top-tier interest rates to a wider range of credit profiles. The promotion runs through the end of September and applies to specific F-150 models only.

Anglo-Saxon burial reveals “unprecedented” secrets: experts stunned by 1,400-year-old grave mysteries

What Your Instinctive Tree Choice Reveals About Your Personality—Experts Explain

- Offer channel: Provided through Ford Credit, not an outside lender.

- Scope: Selected F-150 trims and model years, not all Ford vehicles.

- Timeline: Time-limited, tied to the third-quarter sales push.

A spokesperson confirmed the program exists and said it changes the rate offered, not the basic approval criteria.

Who can get these rates and what the fine print requires

Creators on social platforms flagged that buyers with scores often labeled “subprime” may see rates similar to prime-tier offers. That doesn’t mean every applicant automatically qualifies.

Key qualification points

- Credit score is one factor; Ford uses its own scoring model beyond FICO.

- Income and affordability standards still apply.

- The actual rate depends on loan length and payment terms.

In short, a lower credit score can unlock a better interest rate under this deal, but applicants still face income checks and variable loan pricing.

Buyer and lender risks with easier financing

Making low rates available to higher-risk borrowers can clear dealer lots. But it also raises several concerns.

- Higher default risk: Borrowers with lower scores historically miss payments more often.

- Repo exposure: Dealers and finance arms could see more repossessions if payments lapse.

- No price cut: The promotion reduces financing cost, not sticker price. F-150s still start around $39,000 and can exceed $100,000.

Why Ford may be timing the offer now

Automakers race to shape quarterly sales figures. Promotions near quarter-end can both boost numbers and thin inventory before new model-year vehicles arrive.

- F-150 inventory pressure can prompt short-term incentives.

- Stronger reported sales for a quarter can favor investor sentiment.

- Promotions are a common tactic around model-year transitions.

Data show mixed signals: F-Series sales were up about 12.7% year-to-date, yet August sales lagged 3.4% versus last year.

How this fits into the wider auto market

Ford isn’t the only OEM using aggressive financing. Rival brands launched competitive offers this season to move trucks and SUVs.

- Stellantis’ Ram brand has promoted 0% deals for qualified buyers.

- General Motors’ Chevrolet and GMC advertised similar low-rate offers through September.

- Average new auto loan rates hovered near 9%, while subprime borrowers faced rates around 18–20%.

That backdrop helps explain why an automaker might temporarily compress rate tiers to stimulate demand.

Social media reaction and consumer sentiment

The promotion sparked a viral discussion after a TikTok creator highlighted the change. Viewers split between seeing a smart sales tactic and a symptom of a deeper pricing problem.

- Common complaints: Many say finance terms won’t fix high sticker prices.

- Price vs. finance: Several comments argued the real issue is vehicle cost, not lending.

- Skeptical takes: Others joked the move guarantees work for repo agents.

Online posts also pointed out that loan affordability still hinges on buyers meeting income thresholds, despite the more generous rate bands.